This visual summary of Wellington Management’s 2025 Outlook captures insights on economic and market forces shaping investment results from specialists from across our investment platform.

Throughout 2024, we’ve seen increased fiscal stimulus after every election and subsequent government budget suggesting that, like the market, governments believe central banks have their backs. Fiscal deficits widened exponentially during the COVID crisis to take the slack, but the subsequent nominal growth hasn’t been used to heal those deficits. Therefore, they remain worryingly high in an environment where rates could be cut less than markets and governments currently anticipate — something we’ll be keeping a close eye on in 2025.

Dive deep into five key themes for an uncertain 2025

Sources: LSEG Datastream/G7 cyclically adjusted budget balance as % of potential GDP, OECD (2024), General government deficit (indicator). doi: 10.1787/77079edb-en (Accessed on 11 June 2024) | Chart data: 31 December 1995 – 31 December 2023

Looking forward, we think the familiar paradigm of Fed-led convergence may be ending, with central banks more likely to pursue distinct policy paths. However, a period of prolonged divergence isn’t without precedent — think back to the 1970s. Just as was the case then, growth/inflation trade-offs may take on increasingly local dimensions, meaning rates markets may become more sensitive to national, rather than global, cycles. We don’t think investors have yet priced this in.

Discover what bond divergence means for investors

Sources: Bloomberg Finance L.P. | Data as of November 2024.

For some time, most of the US market has trailed behind select tech mega-caps that have experienced strong earnings growth, thus remarkable gains (thanks AI!). However, in the second half of 2024, earnings growth began to expand owing to wider economic growth, lower inflation, and lower short-term interest rates. In 2025, mega-caps’ earnings will be measured against their own stellar past two years, while the rest of the market has more room to grow, signaling potential stock-picking opportunities.

Consider these five themes for equity investors

Sources: Wellington Management, Bloomberg Finance LLP. Chart from Wellington’s Solutions Group. | As of 11 November 2024. Data represents year-over-year change in EPS (US$/share) for S&P 500 Index and the technology and media industries within S&P 500 Index. | Future quarters are consensus. PAST INDEX OR THIRD-PARTY PERFORMANCE DOES NOT PREDICT FUTURE RETURNS.

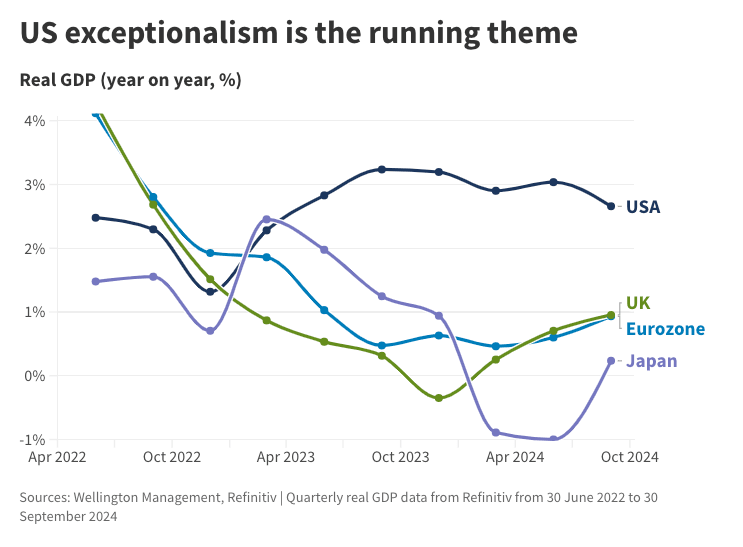

Expectations of deregulation and lower taxes in the next US presidential administration have fed into an ongoing theme of US exceptionalism, which may prompt the question of how long this can last. But, while much of the policy landscape is unknown, the fundamental picture in the US is good — the growth/inflation balance has improved, earnings are strong relative to the rest of the world, and Fed policy is supportive. As such, we believe there’s a case to be made for a moderately overweight view on US equities.

Explore the potential impact of another Trump administration

Gone is the relatively stable economic environment of the 2010s, but the new regime may drive higher security dispersion, macro volatility, and interest rates — all of which could be beneficial for hedge fund performance, if history is any guide.

Learn more about these three drivers of hedge fund outperformance

Sources: Wellington Management | For illustrative purposes only.

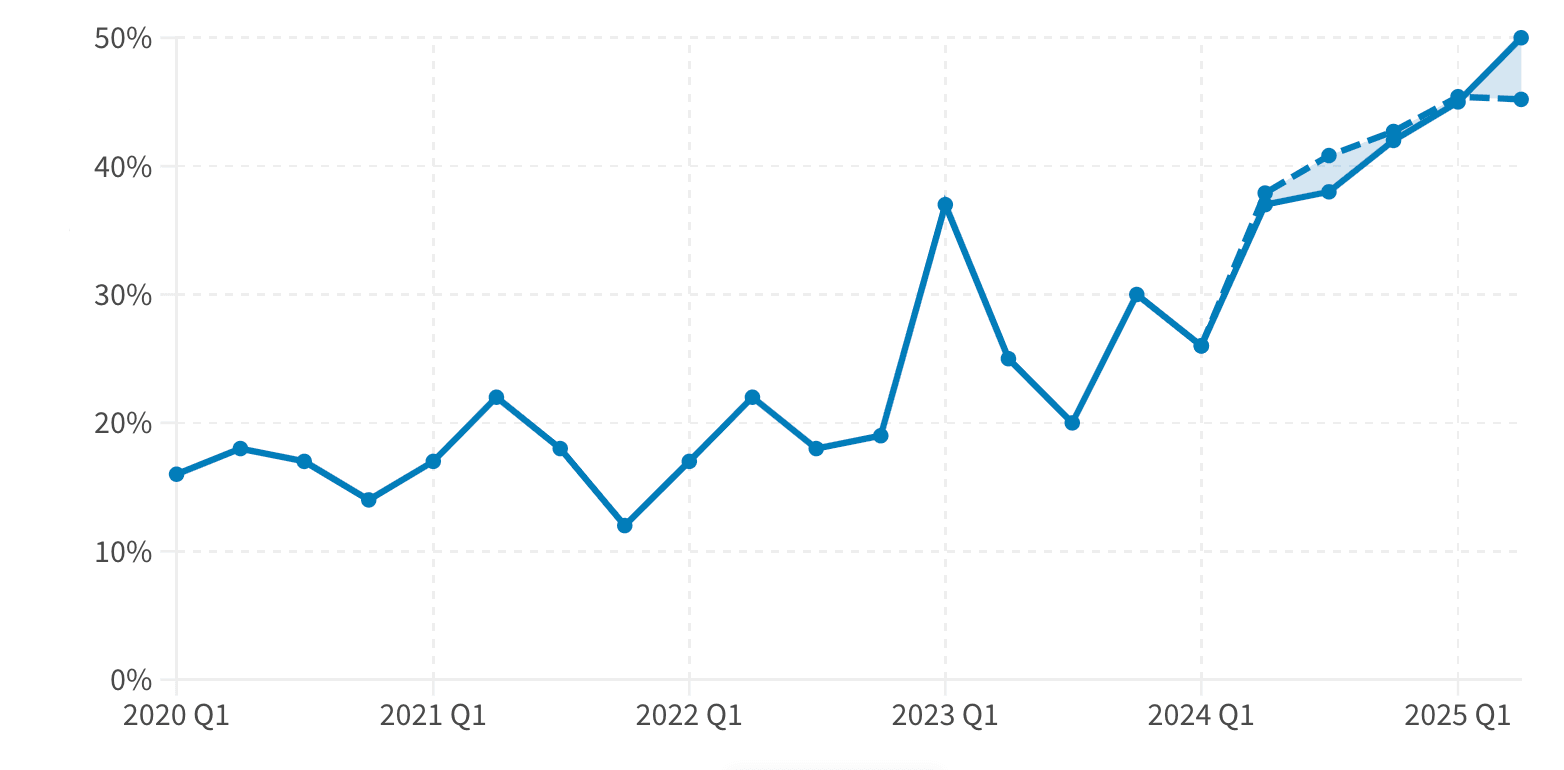

Source: PitchBook as of 9 October 2024. US, Canada, and Europe only. All VC stages. Data from Q120 to Q324 is actual. Data from Q424 to Q225 is estimated using the average growth rate during the prior period (10%).

Many of today’s premier venture capital (VC) players rose to prominence during waves of innovation like the internet, software, mobile, and crypto. So, it’s no surprise that the VC space has played a crucial role in the ascension of the latest disruptive technology, AI. But what's next for AI venture capital? Click and drag on the chart to predict AI VC spending for 2025.

Uncover the role of VC in AI disruption

AI as a % of venture investments

Did you miss an issue? Looking for quick, visual content? Check out our other infographics and spotlights:

Picture This: Economic Forecast in 7 Charts

This visual summary of Wellington’s Outlook captures insights on key economic and market developments from experts across our investment platform, ranging from macro perspectives to latest views on public and private asset classes.

Published: September 2024

Commodities: Entering a scarcity-pricing regime

Is copper the oil of the energy transition? Wellington looks at this commodity’s future, captured in four charts.

Published: June 2024

Geopolitical instability

Equity market concentration

Equity valuations or credit spreads

Risk of recession

Disappointing performance of active management

Justifying exposure to non-US or EM equity

Prospects for private equity or private credit

Unstable asset class correlations

Potential for higher interest rates in next 2 – 3 years

Other